In Islamic values, the family is the smallest unit that bears a great mandate. Children are not merely a source of happiness; they are a trust (amanah) that accompanies the parents' role as leaders. This responsibility is known as Mas’uliyah—a moral obligation for leaders (parents) to ensure the well-being and future of those they lead (their children).

One tangible form of this responsibility is ensuring that children receive the best possible education. Education is the primary provision for a child to grow into a beneficial individual, both economically and spiritually independent.

Mas’uliyah: Why Must Education Be Prepared Early?

Philosophically, parents are the guardians of a child's future. Preparing education funds in a measured way is not about excessive worry over tomorrow, but rather a form of sincere Ikhtiar (effort). In a healthy family concept, parents must strive to ensure their descendants do not grow up in a weak condition, whether in terms of knowledge or finances.

Mature planning is a true expression of love. With ready education funds, parents can provide the best school options for their children without being burdened by debt in the future. This is where synergy between husband and wife becomes crucial.

A Collaborative Way for Husband and Wife to Manage and Save for Education with the Jago Syariah Shared Pocket

The key to successful saving is not just about the size of the income, but how neatly it is managed. A common problem faced by couples is "school money being used for daily expenses" because it is mixed in one account.

The Jago Syariah Shared Pocket serves as a modern solution aligned with the values of openness and transparency. This feature allows couples to have a "shared vessel" for one noble goal: their children's education.

Advantages of the Jago Syariah Shared Pocket

- Full Transparency: Both husband and wife can view the balance and transaction history simultaneously in the Jago application from their respective phones. This prevents "hidden spending" and increases trust.

- Wadiah Yad Dhamanah Principle: Funds are managed according to Sharia principles based on akad. You gain peace of mind because the money is kept without interest.

- Zero Admin Fees: Every rupiah you set aside every month is not cut by monthly fees, allowing the education fund target to be reached faster.

- Separation Based on Intent: You can create different Pockets for each child or each education level. Because There is a Pocket for every good intention.

Detailed Simulation: Timing and Allocation for Education Funds

The success of an education fund depends heavily on when you start. The earlier you begin, the lighter the monthly contribution required. Here is an ideal timing and allocation simulation:

1. Kindergarten fund (Start: When the child is 0-1 year old)

While it may seem premature, the entry fees for private kindergartens are currently quite high.

- Start Time: Immediately after the child is born.

- Allocation Portion: 5% - 10% of joint income.

- Jago Strategy: Create a "Kindergarten Pocket" in Jago Syariah. Use the Auto-Budgeting feature so that on every payday, the funds are immediately locked for the child's future.

2. Elementary school fund (Start: When the child is 2 years old)

Elementary school is the longest stage (6 years). The enrollment fee is usually the first major expense parents feel.

- Start Time: No later than when the child turns 2 (allowing 4 years to save).

- Allocation Portion: 15% of joint income.

- Simulation: If the enrollment target is Rp20 million, the couple only needs to set aside a total of around Rp400,000 per month for 4 years.

3. Junior and senior high school fund (Start: When the child is in 1st grade)

Once the child starts school, do not stop saving. Begin building the fund for secondary education.

- Start Time: When the child is 6-7 years old (start of Elementary).

- Allocation Portion: 10% of income + allocations from annual bonuses or holiday allowances (THR).

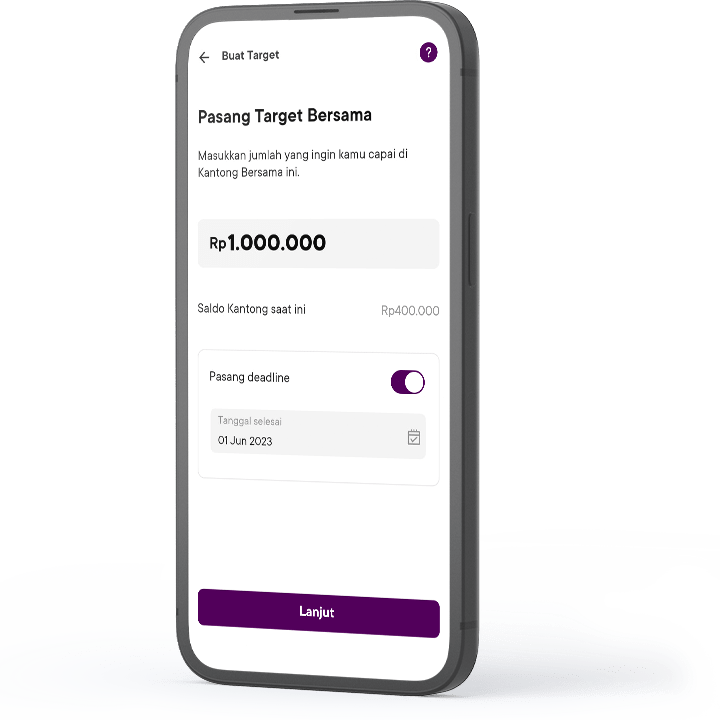

- Jago Strategy: Use the "Target" feature in the Shared Pocket. The application will show the percentage of progress toward the dream school costs.

4. Higher education/university fund (Start: When the child is in 4th grade)

University costs have the highest inflation compared to other levels. Based on BPS data in 2024, higher education expenses increased by nearly 90 percent compared to costs incurred during high school (Source: Hoshizora Foundation).

- Start Time: When the child is 9-10 years old. Do not wait until they reach high school, as the saving window will be too short and burdensome.

- Allocation Portion: Minimum 20% of the family's savings capacity.

- Jago Strategy: Use the Shared Pocket as a long-term instrument. Consistency over 8 years (from 4th grade until high school graduation) will allow the fund to accumulate more stably.

FAQ Regarding Education Fund Preparation

1. Why should education savings be separated into different Pockets?

Psychologically, mixing money makes us feel like we have "plenty of cash," when in reality, that money is designated for school. Separation using the Jago Syariah Pockets ensures that every good intention (education, qurban, Umrah) has its own place.

2. What if the husband and wife have unequal incomes?

Mas'uliyah is a leadership responsibility, but the technicalities can be agreed upon. For example, the husband may cover the enrollment fee (large nominal), while the wife fills the Pocket for monthly tuition or extracurriculars. Transparency in the Shared Pocket makes this division easier.

3. When is the best time to evaluate education savings?

Evaluate once a year. Check if the target school's fees have increased, then adjust the contribution amount in your Shared Pocket to stay relevant with inflation.

A good intention must be accompanied by a jago way. Start fulfilling the mandate of your child's education today with Jago Syariah, because there is a Pocket for every good intention.