Watching your little one grow up is a joy, but as a parent, one thing often triggers anxiety: university tuition. It feels like just yesterday they started kindergarten, and suddenly, you’re staring down the barrel of university fees.

To make matters more challenging, there is the phenomenon of education cost inflation, which often jumps much higher than annual salary raises. Let’s break down the strategy so you can secure their future with peace of mind!

What is the Estimated Inflation for University Tuition?

Reported by Tempo, annual education inflation averaged 1.95 percent as of July 2025. However, university tuition costs alone skyrocketed by 282 percent between 2015 and 2024.

When Should You Start Saving for Your Child's University Fund and Which Scheme Should You Use?

The principle is simple: The earlier you start, the lighter the burden. Don’t wait until your child is in high school to start feeling overwhelmed by higher education fund planning.

1. Long-term scheme (Toddler age)

You have a 10-15 year window. Because the timeframe is long, the monthly amount you set aside doesn't need to be massive, thanks to the maximum balance accumulation effect.

2. Mid-term scheme (Elementary school age)

With only about 5-7 years left, you need to be more disciplined. Aim to set aside at least 15-20% of your monthly income specifically for this post.

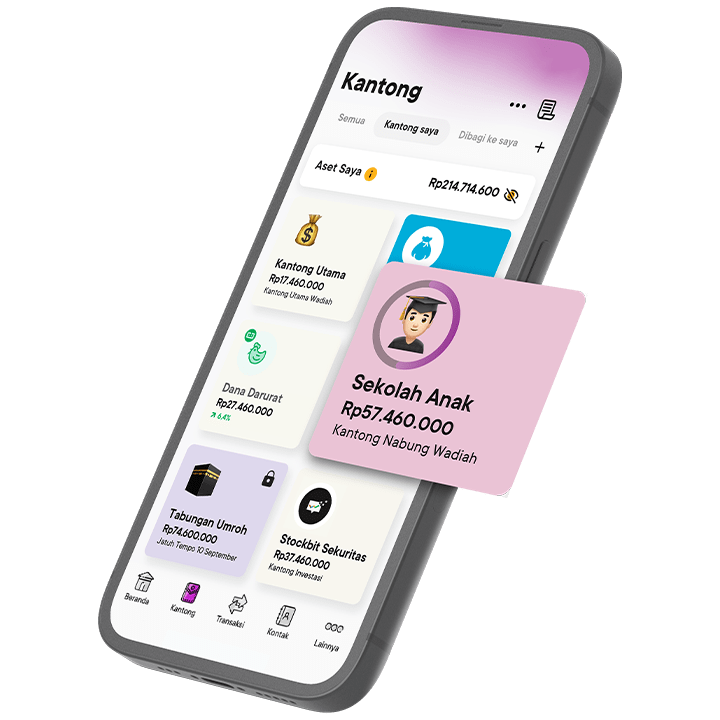

Manage University Funds Seamlessly Using the Pockets in the Jago Application

To ensure the university fund stays safe and doesn’t get "accidentally" spent on online shopping or household needs, you can use the Jago application and its Pockets feature.

Why save for your child’s university tuition in the Jago/Jago Syariah Pockets?

- Clear Fund Separation: Create a dedicated "Pocket" named "University Fund." This money stays separate from your main balance and other spending needs.

- Auto-Budgeting Feature: Set it up so that every payday, your balance automatically moves to the Education Pocket. No need for manual transfers!

Real Example: Calculating Your Target University Fund

To give you a clearer picture, let's look at an example. Suppose your child was just born, and you’re eyeing a university where the total cost (enrollment + tuition until graduation) is currently Rp100,000,000.

If we assume a 10% annual education inflation rate, then in 18 years when your child enters college, the cost won’t be 100 million anymore, but rather:

Estimated Cost in 18 Years: ± Rp555,000,000

The Saving Scheme:

- Start at age 0: You need to set aside approximately Rp1.2 million - Rp1.5 million per month (assuming balance growth or annual bonuses).

- Start at age 12 (Junior High): You would need to save nearly Rp6 million per month to reach the same target!

See the difference? Saving early in a Jago/Jago Syariah Pocket makes securing your child's future much more manageable.

FAQ About Education Funds

1. What are the benefits of saving for university using the Jago/Jago Syariah Pocket feature?

You can have multiple Pockets for different needs. And, if you have more than one child, you can save for each child's education costs in separate Pockets. This allows you to focus on monitoring the growth of each specific fund.

2. What if my child gets a scholarship?

That’s even better! The funds you’ve collected in your Jago/Jago Syariah Pocket can be redirected toward their living expenses during university, thesis research costs, or even as seed capital for them to start a business after graduation.