Being a freelancer does offer many advantages, such as more flexible working hours and you get to be your own boss. However, a freelancer's income can fluctuate, unlike those who work in an office who receive the same amount of salary every month.

Those of you who are a freelancer or want to change professions to become freelancers need to know how to manage finances with income that can go up and down every month.

Just because income is unpredictable, doesn't mean your financial life is also unpredictable. Managing finances properly is an important key to living a happy life. Here are 4 financial tips for freelancers.

4 Financial Tips for Every Freelancer

1. Make a monthly budget

Making a monthly budget is important for everyone, not just freelancers. But, for those of you who are freelancers, it will be easier and more useful if you start with expenses.

Expenses such as monthly bills and daily food needs should be prioritized. You can also include other needs such as entertainment and transportation to meet clients, for example.

After knowing how much you spend each month, it will be easier for you to determine how many projects you should accept and complete, so that you can cover expenses, and you can save the rest of your income.

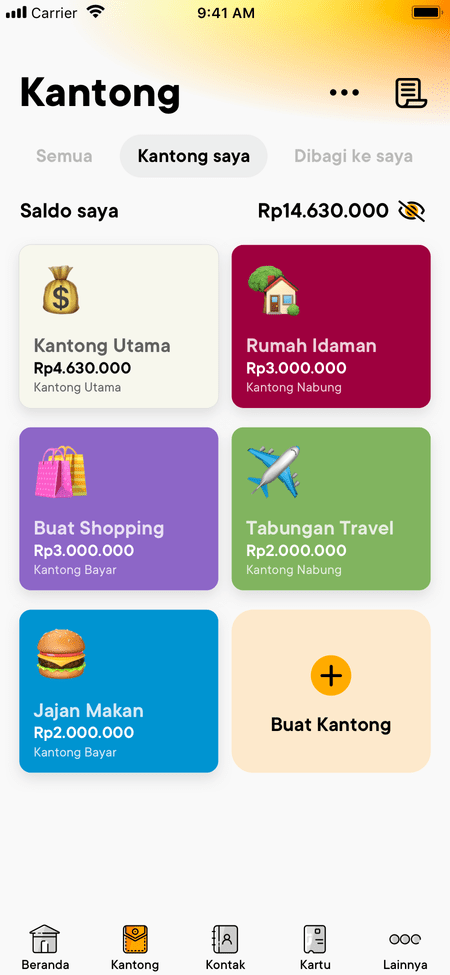

So that managing needs and finances can be easy and practical, you can take advantage of the Jago application. In the Jago application, there is the Pocket feature in the form of the Saving Pocket and Spending Pocket that can be created up to dozens of them to separate various needs. One Pocket is equal to one account. In other words, you can have multiple Bank Jago accounts in the Jago application. You can also allocate funds for each Pocket easily, automatically or manually, and monitor transaction history per Pocket.

2. Build an emergency fund

As a freelancer, having an emergency fund is very important. You need to think about when offers or projects are low. You also need to think about when you have to spend money on something you didn't expect. Not to mention if you have family or dependents.

Emergency fund savings should be kept for emergencies only. In the Jago application, you can put your emergency funds in a Locked Pocket with the shortest locking option (e.g., 14 days) to prevent yourself from using it. You don't have to save a large amount at once.

A Jago Term Deposit is another option to keep your emergency funds. It is suitable for large amounts and doesn't have penalty fees for closing it at any time.

3. Save for retirement

Being a freelancer allows you to work until whatever age you want. When office employees are no longer able to work, you can still. You can also decide to stop working early and enjoy life without having to work anymore.

Whatever decision you make, if you want to be able to retire comfortably, you should start saving for retirement early.

To save for retirement consistently every month, you can use the automatic saving feature in the Jago application. Savings will be effortless because it is automatic.

4. Separate business and personal bank accounts

It will be much easier for you to know exactly how much money you receive from working as a freelancer when you separate your business and personal bank accounts.

Not only income, by separating business and personal bank accounts, it will also make it easier for you to monitor business expenses. This will be useful later when you have to fulfill your income tax reporting obligations.

Having two different bank accounts sounds complicated. But, it doesn’t have to be complicated if you already have a Jago account. With Jago, you can have multiple bank accounts in one account. The trick is to create different Pockets. Each of these Pockets will have a separate account number, as explained above.

Don't worry, Jagoans, having multiple account numbers doesn't mean you will be subject to high monthly admin fees. Bank Jago frees you from monthly admin fees. This means that if you have 40 Pockets (40 different accounts), all of them are free of monthly admin fees.

Enjoy being a freelancer who is good at managing finances.