Having debt is often seen as something negative, especially if you are unable to pay it off or repay it. However, not all debt is bad. There are 2 types of loans that you should know, namely productive loan and consumptive loan. Which type is better and which is best avoided?

Differences between Productive and Consumptive Loans

You can probably guess from the name which needs to be avoided and which is not a problem if it is paid off as it should be.

What is a productive loan?

A productive loan is used for productive needs. So, a person's goal in borrowing money or taking on debt is usually to make money. The hope is that the income earned will be large. Thus, on the one hand, this income can be used to pay off or repay debts and on the other hand it can be used to meet living needs, save, or other purposes.

Examples of productive loans

So what are some examples of productive loans? For example, someone who wants to start a business but doesn't have enough capital. Another example is borrowing money to buy business equipment so that the business can grow or as capital for business expansion for business growth.

What about people who apply for a loan to buy a motor vehicle such as a car or motorbike and then use it to earn income? This example is also included as productive.

What is a consumptive loan?

How is a consumptive loan differentt? The difference is very big. It is the total opposite. Consumptive debt occurs when someone borrows money to meet individual or household needs. In other words, loans are not used to make a profit.

What are examples of consumptive loans?

There are many examples that are often found in society. For example, someone who borrows money to spend on extravagances or fulfill a lifestyle such as buying expensive bags and shoes, staying in luxury hotels. Consumer debt often arises due to prestige and FOMO. Consumer debt can also occur because someone wants to buy something beyond their means.

Thus, consumptive debt should be avoided because its main purpose is only to fulfill wants. Meanwhile, you can have productive debt but still take into account several factors such as financial ability to pay debt, debt ratio and loan interest amount.

How Much Debt Can You Have?

Many of you may be wondering, how much debt can you actually have? Is there a maximum limit so that debt can still be handled properly and does not affect current financial conditions?

As seen on Investopedia, there is a general rule that can be used as a reference, namely rule 28/36. According to this rule, home-related expenses, such as mortgage payments, home insurance, and property taxes, cannot exceed 28% of gross income.

And, at the same time, total expenses for all housing-related expenses and other debts should not exceed 36% of gross income. Examples of other debts in question are credit card bills and car loans.

How to Avoid Consumptive Debt?

To avoid consumptive debt, there are some ways you can do. But, you really have to be disciplined in doing it.

1. Separate your budget for fun or wants into a separate account

Of course you can buy something you like, as long as it is within your means. For example, you can allocate 30% of your monthly income for wants. The remaining 50% is for needs and 20% for savings. The 50-30-20 budgeting method is just one commonly used method.

However, budget allocation does not have to be strict like that. The numbers can be adjusted again. For example, if it turns out that your main or priority needs, such as paying monthly bills and groceries, only take up 40% of your salary, then the remaining 10% can be allocated to wants or even saved for financial goals (Moneyfesting).

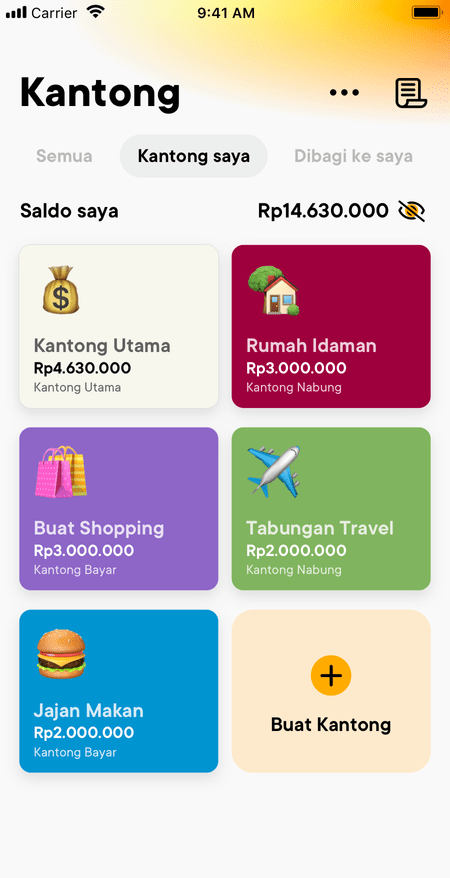

The Jago application makes it possible and easy for you to create multiple accounts without monthly admin fees to manage many needs. Create Jago Pockets for all needs that must be met. 1 Jago Pocket has 1 account number. The budget for wants or fun can be separated into a separate Jago Pocket that has been created.

2. Set daily transaction limits for debit card use the way you want

Apart from budgeting discipline with the Pocket, to help reduce consumer debt, make sure you shop using a debit card, not a credit card.

If you already have a Jago Visa Debit Card or Jago GPN Debit Card, you can set daily transaction limits, such as online transactions, transactions at EDC machines and transactions via PayWave. Setting daily transaction limits can be done directly via the Jago application. Each Jago debit card you have can have its own limit set, just the way you want.

You can read other effective ways to avoid debt in this article.

How to be Jago at Paying Off Productive Debts

To ensure you pay off your debts or installments on time, here’s how to do it.

1. Allocate budget regularly

So that debts or installments can be paid on time, the first strategy is to budget in a disciplined manner. If there is only 1 debt to pay off, you can create 1 Jago Pocket for this. If there are several installments that must be paid every month, you can create several Jago Pockets according to your needs. Make sure every month you move funds into each Pocket for debt payments or installments.

Want something practical and hassle-free? Use the Auto-Budgeting feature in each of your Pockets in the Jago application. Set the frequency and amount. This way, money will move automatically. You can pay debts or installments on time with the funds that have been prepared.

2. Use the Plan Ahead feature to pay debts or installments on time, just the way you want

After budgeting funds to pay existing debts or installments, for timely and more practical payments, you can use the Plan Ahead feature in the Jago application.

With the Plan Ahead feature, it is easy for you to schedule recurring or routine payments or transfers so you don't miss them. Payments will also run automatically according to the time you have specified.

With Jago, managing finances and paying debts become easier and more practical, just the way you want.