When the sacred vow is spoken, a husband and wife not only unite two hearts but also their future and financial responsibilities. Building a household is a journey demanding transparency and aligned vision, especially in managing wealth. Modern life often traps us in a material race, making us forget the essence of every Rupiah that enters the home.

For Muslim couples, the challenge is deeper: how to ensure every expense, every saving, and every investment not only yields profit but also brings blessings? The answer lies in the fundamental understanding of our role as managers of the wealth entrusted by Allah SWT.

The Concept of Wealth in Islam: Not Our Property, But a Trust and a Test

Wealth in Islam is never considered absolute ownership, but rather a trust entrusted by Allah SWT. This concept distinguishes the Muslim view of wealth from the conventional one.

1. Wealth is a trust

The Qur'an affirms that wealth is a test for humanity, as stated in Surah At-Taghabun verse 15: "Indeed, your wealth and your children are only a trial (for you)..." (Source: Republika). We only act as managers, and one day we will be held accountable for how we acquire and spend it.

2. The obligation to share

The private wealth of a Muslim is recognized as carrying the rights of others. This is the basis for the obligation of Zakat, Infak, and Sadaqah.

3. Wealth must be productive and halal

The management of wealth must comply with religious teachings, and it should ideally be channeled into sectors that are beneficial to the community.

With this understanding, managing family finances for a husband and wife means managing the trust of Allah. This makes the commitment to the following budget posts extremely fundamental.

How to Manage Family Finances: 5 Fundamental Budget Posts for Husband and Wife to Agree Upon

So, how can a husband and wife divide the budget so that all worldly obligations are fulfilled and hold spiritual value? These five budget posts serve as a practical guide for couples to agree upon.

1. Primary priority: Basic obligation

- Focus: Ensuring the family's primary needs (food, shelter, clothing, education, health) are met reasonably and adequately.

2. Freedom from conflict: Debt repayment

- Focus: Paying off family debts (especially those that are productive or for emergencies) and avoiding new debt. The couple needs to be open about the total debt, set a priority for which debt to pay off first, and establish it as a joint monthly target.

3. Investment for the hereafter: Zakat, infak, sadaqah

- Focus: Allocating mandatory funds (zakat) and wealth purification funds through infak and sadaqah. The Zakat budget should be separated at the beginning (saving first). The couple can agree on a joint budget for voluntary infak (sunnah charity), embedding the value of good deeds into the family's cash flow.

4. Asset protection: Halal savings and investment

- Focus: Growing and protecting wealth to achieve financial independence and the family's future (retirement fund, education fund) through Sharia-compliant investment instruments. The couple must agree on a joint risk profile and specific fund targets. Investment should be viewed as a mutual effort to secure the future of their descendants.

5. Test of self-control: Lifestyle and comfort

- Focus: Spending on recreation, refreshing, or purchasing secondary items. This post becomes the main test for the couple to avoid being wasteful. The couple needs to set a joint spending limit on this post to avoid excessive lifestyle choices, ensuring expenditures remain balanced and do not cause jealousy.

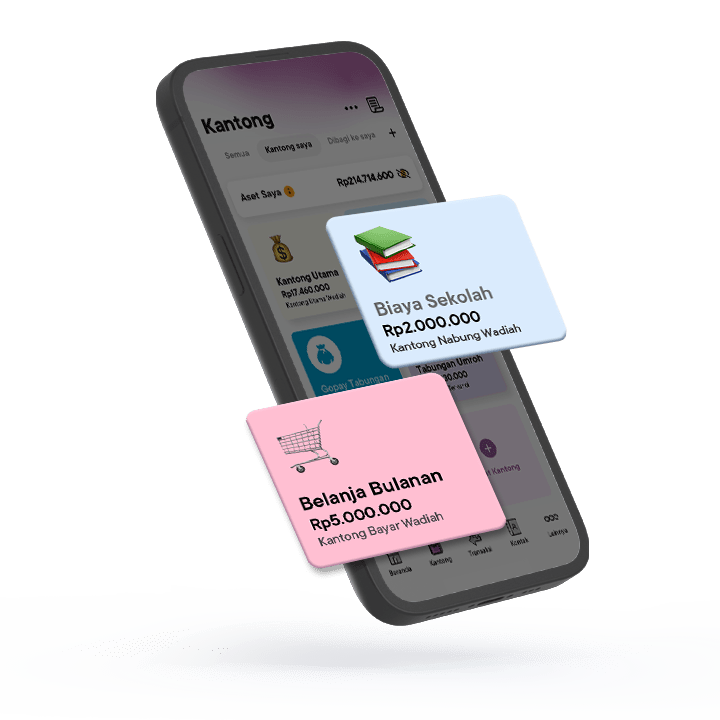

The Jago Syariah Pockets: The Way to Manage Trust-Based Wealth in a Sharia-Compliant and Goal-Oriented Manner

How can modern Muslim couples ensure their entrusted funds are segregated, Sharia-compliant, and disciplinedly allocated across the five budget posts? The answer lies in using the Jago Syariah Pockets, which transforms the concept of Harta Amanah into an easy daily practice.

1. Goal-oriented saving with Wadiah akad

Every Saving Pocket or Spending Pocket in Jago Syariah is based on Wadiah Yad Dhamanah akad (safekeeping without interest), ensuring funds for various needs and expenses are managed according to Sharia principles. Creating separate Saving Pockets for specific goals (retirement, child education, etc.) is a tangible way to secure the entrusted wealth from being used for non-priority expenses.

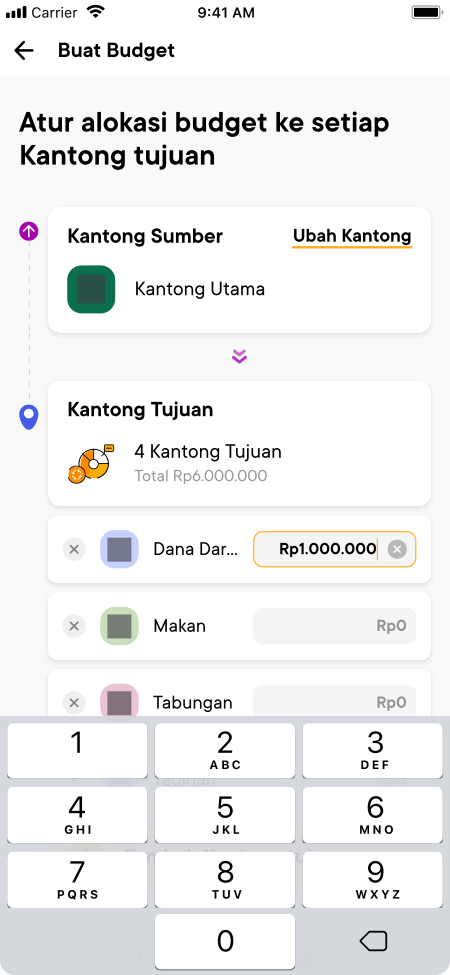

2. Automation for consistency and sharing via Auto-Budgeting

The primary financial obligations and investments for the hereafter cannot be missed. Use the Jago Syariah Auto-Budgeting feature to set automatic transfers of specific amounts to various destination Pockets. This helps build self-discipline in managing family finances while fulfilling the obligation to share.

Example Allocation of 5 Posts with the Jago Syariah Pockets

|

Budget Post |

Estimated Percentage |

Jago Syariah Pocket Created |

Jago Syariah Feature |

|

1. Primary Needs |

50% |

Spending Pocket (Shared Pocket) for 'Kitchen Needs' |

Shared Pocket for joint transparency, main cash flow allocation. |

|

2. Debt Repayment |

10% |

Spending Pocket for 'Home Installment' |

Auto-Budgeting for automatic fund allocation and Plan Ahead feature for timely payment. |

|

3. Investment for Hereafter |

5% |

Spending Pocket for 'Monthly Sadaqah' |

Auto-Budgeting to a donation Pocket, ensuring charity is not forgotten. |

|

4. Savings/ Investment |

25% |

Savings Pocket for 'Child Education', 'Retirement', 'Emergency Fund' |

Separate savings according to purpose. |

|

5. Lifestyle |

10% |

Spending Pocket for 'Family Entertainment' |

Jago Syariah Debit Card linked to this Pocket, limiting overspending. |

With the Jago Syariah Pockets, the management of family wealth becomes a digitally efficient, measurable, and blessed practice, allowing you and your partner to focus on spiritual and worldly goals.

Quick Q&A on Managing Household Finances with the Jago Syariah Pockets

1. Does Jago Syariah charge a monthly admin fee?

No. Jago Syariah does not charge monthly administration fees for the Pockets you own, ensuring the money allocated for saving and obligations remains intact.

2. How does the Shared Pocket help maintain marital harmony regarding finances?

The Shared Pocket encourages full transparency. The husband and wife can see all cash flow in real-time, eliminating potential suspicion or conflict due to secret debts or hidden expenses, which is key to marital harmony.

3. What are the main requirements for my investment to be Sharia-compliant?

Besides being interest-free, the investment must be free from gharar (uncertainty/excessive speculation) and maisir (gambling), and must not fund prohibited sectors.

4. How do the Jago Syariah Pockets help me avoid wasteful behavior?

With the Pocket and Auto-Budgeting features, you 'bind' your money to the right purpose before spending. You physically separate daily spending funds from your savings funds, which prevents wasteful behavior and helps you better manage household finances.