The end of the year is often synonymous with "windfall income"—unexpected income or extra money that comes in large amounts outside of the regular monthly salary. This additional fund, if not managed well, can be spent instantly on consumptive expenses. However, with everything having its own Pocket, every rupiah from this unexpected fortune can be allocated to the right and prioritized category.

Types of Windfall Income or Additional Earnings Common at the End of the Year in Indonesia

In Indonesia, there are several types of extra income most commonly received towards the end of the year.

1. Religious holiday allowance (THR) for Christmas

- Definition: A mandatory fund provided by the company to employees ahead of a Major Religious Holiday. For those celebrating Christmas, THR is usually disbursed in December.

- Significance: Often the second largest fund after the annual salary, used for going home (mudik), celebrations, and specific holiday needs.

2. 14th salary (additional bonus)

- Definition: In the private sector, this is often realized as an end-of-year bonus or a performance incentive (e.g., annual bonus or tantiem).

- Significance: As an appreciation for a full year's performance. The amount can vary, from one month's salary to a certain percentage of the company's profit.

3. Higher salary due to PPh 21 year-end adjustment (TER Scheme)

- Definition: The change in the calculation method for Income Tax (PPh) Article 21 using the Effective Average Rate (TER) scheme results in a larger tax deduction during normal months. However, in the December salary calculation, a year-end adjustment occurs to calculate the total PPh owed for the entire year. If the total PPh already deducted (accumulation from January to November) is greater than the annual PPh owed, the difference will be returned, making the net salary for that month higher.

- Significance: This salary increase purely comes from the overpaid tax being returned, which is the employee's right.

4. Large sales commissions or incentives

- Definition: Extra income for employees working in sales, marketing, or projects who achieve significant targets at the end of the accounting period (end of the year).

- Significance: It is not always mandatory, but it is often significant for target-based workers.

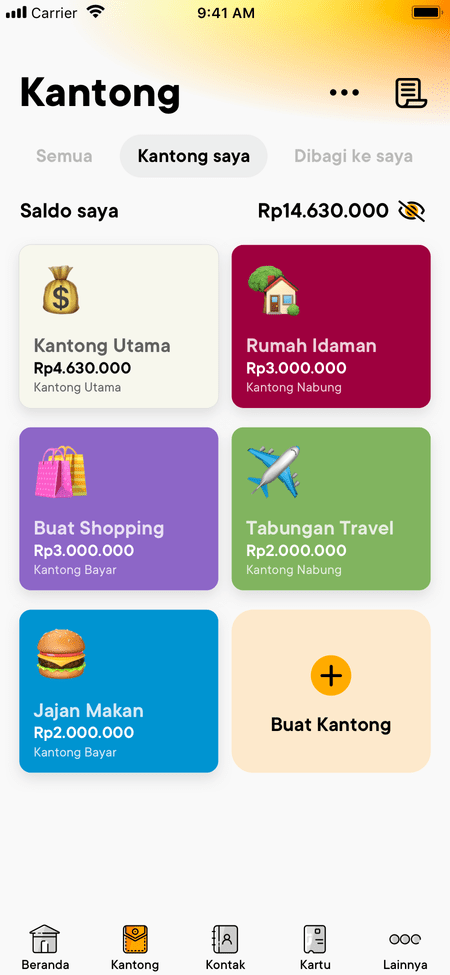

Why Does Extra Money Need Many Jago Pockets?

The Pocket concept in the Jago application is a practical implementation of the traditional envelope method often used to separate money.

The Jago Pockets are important for managing large funds because they:

- Prevent Leaks: Extra funds mixed with the main account tend to be considered 'leftover' money and are prone to being used for impulsive buying or unplanned consumptive spending.

- Clear Priorities: Each Pocket has a specific purpose (financial goals). This makes it easier for you to allocate money based on priority.

- Allocation Visualization: You can clearly see what percentage of the funds are allocated for investment, savings, and self-reward. This helps in financial planning and budgeting.

Simulation of Additional Income Allocation for Financial Goals

Here is an example of allocating windfall income (e.g., amounting to Rp10,000,000) using the Pocket feature with a smart priority approach.

|

Priority |

Pocket Name |

Percentage |

Amount Allocated |

Financial Goal |

|

1.Mandatory |

Debt & Installment Payment Pocket |

30% |

Rp3,000,000 |

Paying off high-interest debt (credit card, paylater) or accelerating mortgage/vehicle installments. |

|

2.Future |

Long-Term Investment Pocket |

25% |

Rp2,500,000 |

Allocated to term deposits, mutual funds, stocks, or other investments such as gold. Increasing net worth. |

|

3.Security |

Emergency Fund Pocket |

20% |

Rp2,000,000 |

Adding to the emergency fund balance until it reaches the target of 6-12x monthly expenses. |

|

4.Needs |

Year-End Needs Pocket |

15% |

Rp1,500,000 |

Costs for Christmas/New Year celebrations, gifts, planned self-reward expenses, and year-end holidays (including staycation). |

|

5.Optional |

Education/Training Fee Pocket |

10% |

Rp1,000,000 |

Investing to improve skills, purchasing online courses, or children's school fees. |

|

TOTAL |

100% |

Rp10,000,000 |

By creating five different Pockets, your funds are not only secure but also productive. This is a brilliant strategy for financial management and maximizing the use of additional money.

Utilize Windfall Income Wisely Because Everything Has Its Own Pocket

Year-end windfall income is a golden opportunity to leap further in achieving your financial goals, not merely an accessory for seasonal shopping. Whether it's THR, a bonus, or the surplus from overpaid PPh 21 due to the TER scheme, with a disciplined Pocket strategy, you transform this extra income from a 'come-and-go' fund into sustainable capital.

With everything having its own Pocket, every goal—from debt, future investment, to small self-rewards—can have its own separate Pocket. By separating these funds, you ensure that important categories are fully funded, while consumptive spending remains controlled. A happy year-end is a planned year-end, and the best planning starts with smart Pocket separation.

Q&A on How to Use Year-End Additional Money

1. What is the difference between windfall income and monthly salary?

Monthly salary is routine and predictable income. Windfall income is extra, non-routine income (e.g., performance bonuses, THR, large commissions, or PPh 21 refund), and ideally should be allocated for long-term goals (savings, investment, debt) so that it isn't spent entirely on consumption.

2. Is it okay to use windfall income for self-reward?

Absolutely! However, self-reward must be allocated within a planned percentage (such as the Year-End Needs Pocket) after prioritizing obligations (debt) and the future (investment & emergency fund). This is called rewarding yourself responsibly.

3. How do I choose which Pocket should be prioritized?

Always follow a healthy financial priority sequence:

- Pay off high-interest debt (especially consumptive debt).

- Strengthen the emergency fund (up to a safe limit).

- Investment (for fund growth).

- Urgent needs/wants (including self-reward).