For a long time, the concept of zuhud has often been misunderstood as an antipathy toward wealth or letting oneself live in deprivation. In reality, zuhud does not mean owning nothing; rather, it means ensuring that your possessions do not own your heart.

Preparing for old age by saving for a Sharia-compliant retirement fund is not a sign of fearing the future or lacking trust in one’s destiny. On the contrary, it is a form of the highest responsibility—to maintain one's dignity and ensure one does not become a burden to others in the twilight years.

Why is Retirement Preparation Part of Zuhud?

1. Financial independence as honor (Marwah)

By having a sufficient retirement fund, a person preserves their dignity and avoids burdening their children or grandchildren, effectively breaking the "Sandwich Generation" cycle.

2. Focus on worship in old age

Old age should be a time to increase social and spiritual activities. Without financial anxiety, one can be more devoted (khusyuk) without worrying about the rising costs of living.

3. Wise risk management

Managing future risks is a form of effort (ikhtiar). Zuhud teaches us to "tie the camel" first before surrendering completely to the Almighty.

Also read: What Major Expenses Await You When Retiring at Your Own Home?

Managing Your Retirement Fund Sharia-Style: There’s a Pocket for Every Goal

To manifest zuhud, a neat financial management system is required. Having a Pocket for every goal or need, Jago Syariah allows you to separate operational funds from future funds so they don't get mixed up. You can utilize three main Sharia-compliant instruments:

1. Saving Pocket with Wadiah Yad Dhamanah akad (Emergency and liquidity)

Use this Pocket to store funds that must always be accessible. With Wadiah Yad Dhamanah akad, your money is safe, free from monthly admin fees, and can be withdrawn anytime without penalties. This is the foundation for storing living cost reserves or emergency health funds for old age.

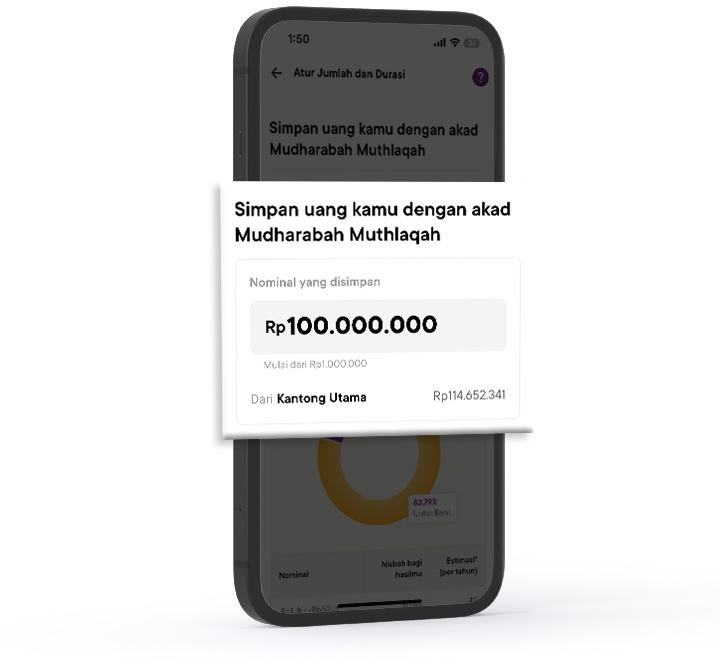

2. Sharia Deposit Pocket with Mudharabah Muthlaqah akad (Value protection)

For funds that have accumulated but won't be used in the medium term (1-3 years), move them to a Sharia Deposit. Using Mudharabah Muthlaqah (profit-sharing) akad, you act as the capital owner and Jago Syariah acts as the manager. With a profit-sharing ratio, the value of your money continues to grow stably and halally to combat inflation.

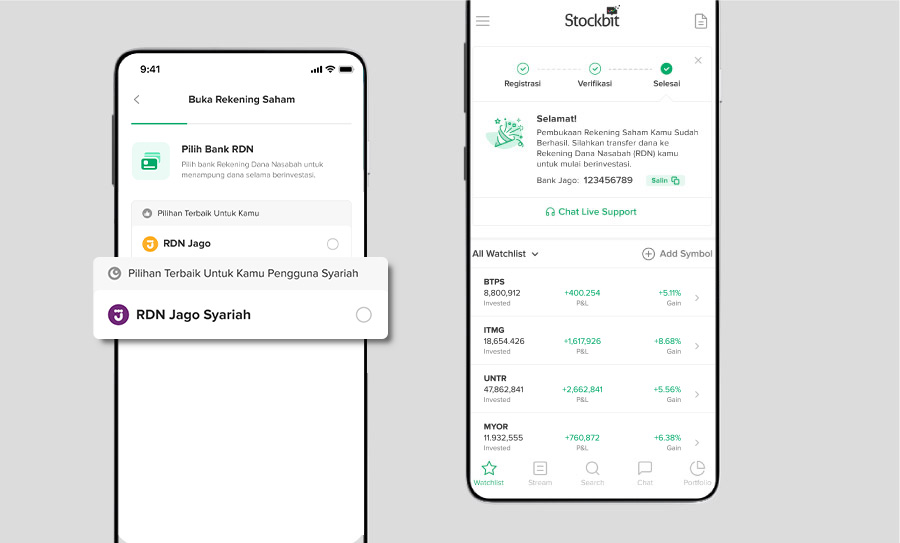

3. Jago Syariah RDN Pocket: Alternative investment options with Bibit and Stockbit

Beyond savings, you have alternative options to optimize your retirement fund through the capital market. The Jago Syariah RDN (Investor Account) acts as a direct bridge integrated with the investment ecosystem:

- Saving in Mutual Funds via Bibit: You can connect Jago Syariah with the Bibit application to buy Sharia mutual funds regularly using the Jago Autodebit payment method. Your investment funds are monitored directly in the Jago application. If you upgrade to Bibit Plus, you have more diversification options using your Jago Syariah RDN.

- Investing in Stocks via Stockbit: The balance in your Jago Syariah RDN Pocket can be used instantly to buy Sharia-compliant stocks on Stockbit. There is a Sharia indicator (crescent moon icon) to ensure the companies you buy are listed in the Sharia Securities List (DES).

- Digital Efficiency: All fund transfers for these investments happen in real-time and are free of admin fees, ensuring every cent you set aside immediately works as a future asset.

Complete Simulation: Retirement Savings Strategy with the Jago Syariah Pockets

How does this division work in practice? Let’s assume the following profile:

- Current Age: 30 Years Old

- Target Retirement Age: 55 Years Old (Time remaining: 25 Years)

- Retirement Fund Target:Rp3 Billion

Here is the breakdown of monthly allocations and projected results:

|

Instrument |

Monthly Allocation |

Role in Old Age |

Estimated Result (25 Years) |

|

Spending Pocket (Wadiah) |

Rp1,000,000 |

Liquid funds for urgent needs. |

Rp300 Million |

|

Sharia Deposit (profit sharing equal to 4% p.a. assoc.) |

Rp1,500,000 |

Value protection with stable profit-sharing. |

Rp770 Million |

|

RDN Pocket (Bibit/Stockbit) |

Rp1,500,000 |

Long-term asset growth (10% assoc.). |

Rp1.99 Billion |

|

Total Monthly Savings |

Rp4,000,000 |

Independent Old Age Effort |

± Rp3.06 Billion |

*The final results in the Deposit and RDN Pockets are influenced by the compounding effect over the 25-year period.

FAQ About Saving Money for Retirement

1. Is saving for retirement a sign of lacking trust in God (Tawakal)?

Absolutely not. Tawakal is surrendering oneself after putting in the maximum effort. Preparing for old age is a part of that effort (ikhtiar) to maintain one's dignity.

2. What is the main difference between Wadiah and Mudharabah akad?

Wadiah is a pure deposit, while Mudharabah is a business partnership where you receive a profit-share from the fund management (as seen in the deposit simulation above).

3. Why should I use the Pockets to prepare my retirement fund?

To make you more psychologically disciplined and have purpose when saving money. By separating retirement funds into specific Pockets, you won't accidentally spend your old-age money on current consumptive needs.

Preparing for the future doesn’t mean we love the world excessively; rather, it is a form of gratitude for our current sustenance by managing it trustworthily (amanah). With an organized financial system, you no longer need to worry about old age. Believe that There is a Pocketfor every good intention. By separating today's needs from tomorrow's hopes, you are practicing zuhud—peace in the heart, organized in the Pocket.