In the midst of a dynamic economy and rising medical inflation, maintaining financial health is no longer just about how much you earn, but how strong your "safety net" is. The 360-Degree Protection concept ensures that every aspect of your life is comprehensively covered, so your savings aren't wiped out when risks occur. Here is the essential checklist and fund allocation strategy using the Jago Pockets.

5 Essential Self-Protection Checklists for 2026

1. Emergency fund

Your first line of defense before insurance. It is vital for non-medical risks, such as layoffs or sudden asset damage.

2. Health insurance (two-layered)

Hospital cost inflation in Indonesia reaches 10-14% annually (Source: Kompas).

- Layer 1: BPJS Kesehatan (Mandatory as basic government protection).

- Layer 2: Private/Additional Health Insurance (Crucial for faster hospital access, private room options, and higher coverage limits).

3. Life insurance

Highly critical if you are the primary breadwinner. Life insurance provides peace of mind, ensuring that the family left behind has the funds to continue their livelihood or settle any outstanding debts.

4. Critical illness insurance

Unlike standard health insurance, critical illness insurance provides a lump-sum cash payment if you are diagnosed with a severe illness (cancer, heart disease, etc.). This cash can be used for living expenses while you are unable to work.

5. Asset insurance for property and vehicles

Protects your productive assets (such as your home or vehicle) from risks like fire, natural disasters, or accidents.

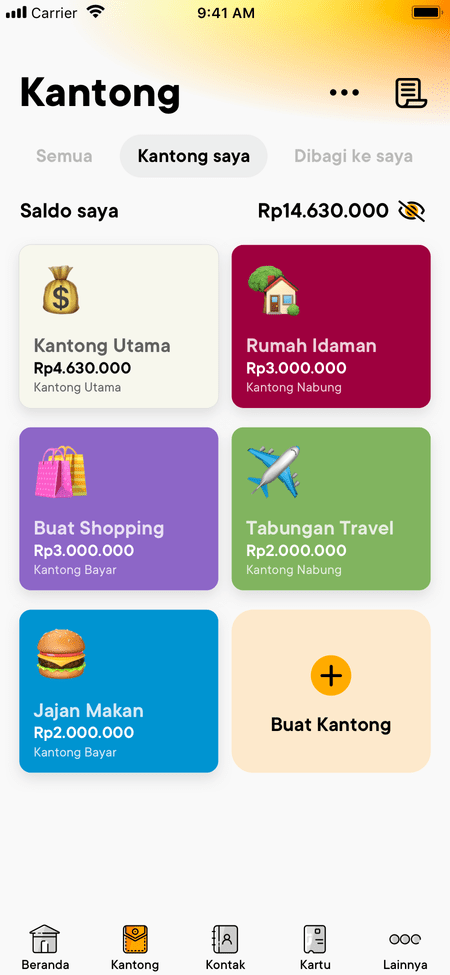

Separate Every Need with the Jago Pockets: Simplify Saving for Emergency Funds and Insurance

With Bank Jago, you can separate each protection need using the Jago Pockets to ensure your funds don't get mixed up. Below is a monthly allocation simulation (assuming a total budget of Rp2,000,000 dedicated to emergency funds and various insurances). Set up one Pocket for each type of protection.

|

Jago Pocket Name |

Protection Type |

Monthly Allocation |

Primary Function |

|

1. Emergency Pocket |

Rp600,000 |

A "spare tire" for unexpected events. |

|

|

2. Health Plus Pocket |

BPJS + Private Insurance |

Rp650,000 |

Combined BPJS fees & private health insurance premiums. |

|

3. Life/Legacy Pocket |

Life Insurance |

Rp250,000 |

Ensuring the livelihood of your heirs. |

|

4. Critical Care Pocket |

Critical Illness |

Rp300,000 |

Cash for recovery in case of severe illness. |

|

5. Asset Guard Pocket |

Vehicle/Property Insurance |

Rp200,000 |

Set aside monthly to pay for annual premiums. |

|

TOTAL |

Rp2,000,000 |

Step-by-Step Guide: Saving for Emergency Funds and Insurance with the Jago Pockets

To build all the protection plans mentioned above, you can start managing your funds with discipline using the Jago Pockets.

- Create Jago Pockets in the application. Since you can create multiple Pockets, you can set up five dedicated Pockets specifically for your protection needs.

- Personalize each Pocket. You can use the names as listed in the table or give each Pocket a custom name that suits your preference.

- Allocate your budget automatically using the Auto-Budgeting feature. Set the specific amount and transfer frequency according to your financial plan.

FAQ: Insurance, Emergency Funds, and the Jago Pockets

1. Why do I need additional insurance if I already have BPJS?

BPJS provides excellent basic coverage. However, private health insurance offers extra comfort, such as private rooms and faster administrative processing without long queues.

2. Should I keep my emergency fund in a Jago Pocket?

Highly recommended. You can use the Locked Pocket feature to prevent impulsive spending while earning competitive interest to combat inflation. The Locked Pockets can be locked for as short as 14 days. Once you’ve saved a significant amount, you can move your fund to a Jago Term Deposit, which has no withdrawal fees if you need to liquidate it before the maturity date.

3. When is the best time to start this protection?

Today. Insurance premiums are much cheaper when you are young and healthy; delaying means paying higher premiums in the future. The same applies to your emergency fund—the sooner you start, the faster you’ll reach your financial safety net.