Many newlyweds find that one of the biggest challenges after marriage is aligning their financial goals. Which comes first, having children or buying a house? What is the ideal emergency fund for a family? When should we start saving for a child's education? This confusion is normal, but there's no need to panic.

To help you and your partner get started, there are 7 financial baby steps you can implement, which are inspired by Dave Ramsey’s baby steps. With these simple steps, you can build a strong financial foundation and achieve all your dreams together.

7 Baby Steps for Newlyweds in Family Financial Planning and Management

1. Create the 'Starter Pack'

Collect the first Rp20 million as a financial "starter pack." This fund acts as a buffer ready for unexpected needs, such as a flat tire, an unexpected doctor's fee, or minor home repairs.

2. Live debt-free

Before taking further steps, pay off all consumptive debts (such as credit card debt or personal loans). You can use the snowball method: pay off the smallest debt first to build momentum, then use the money that was previously going towards that debt payment to pay off the next debt.

3. Build a strong foundation

Once the debt is paid off, it's time to build a strong foundation. Save 3 to 6 months of your family's total living expenses. This fund is the primary safety net for major misfortunes like job loss.

4. Small drops become an ocean

Once the foundation is solid, start investing. Set aside 15% of your combined income for retirement savings. The sooner you start, the greater the power of compounding works.

5. Small step, big leap

The cost of children's education increases every year. Don't delay. Start saving for your children's education now, even before the child is born. Although the amount may be small, consistency is key.

6. Roof paid off, door opened

This is a crucial step. Pay off your home mortgage as quickly as possible. With a paid-off house, you have a solid personal asset, and your monthly expenses will be much lighter.

7. Rich in wealth, rich in meaning

After all the steps above are achieved, you are not just rich in wealth, but also rich in meaning. Use the wealth you have built to do good, whether by helping others or realizing bigger dreams for the community.

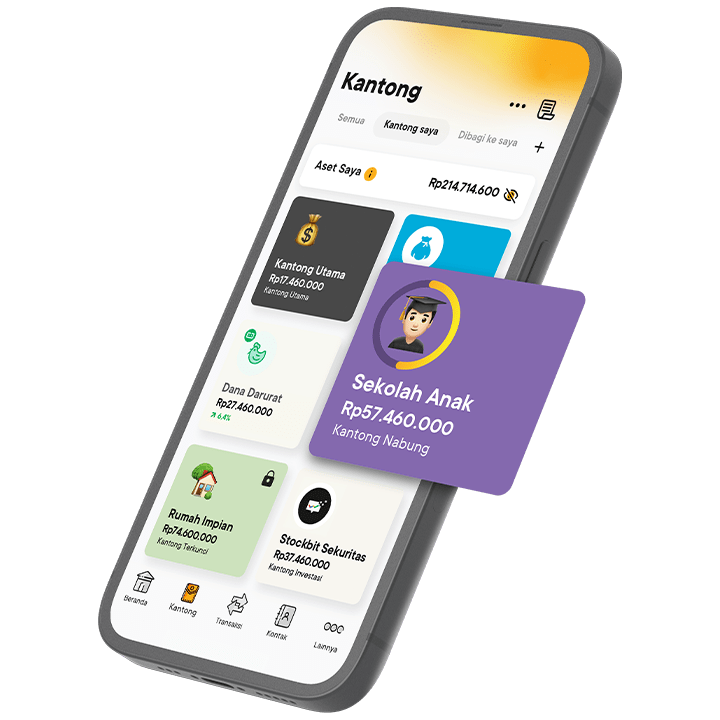

The Jago Pockets: The Easy Way for Newlyweds to Manage Household Finances

The 7 baby steps above will feel much easier with the Saving Pockets, Spending Pockets, and Shared Pockets. These features are the ideal solution for family finances because they allow you and your partner to give money a clear purpose and manage all expenses and savings transparently.

Simulation of the Jago Pocket Usage for Each Baby Step

- Baby Step 1: Create the "Starter Pack"

- Use the Saving Pockets: Create a Saving Pocket named "Starter Pack Fund." Transfer Rp20 million to this Pocket.

- Reason: The Saving Pocket helps separate this fund from daily money, preventing it from being used for unnecessary expenses.

- Baby Step 2: Live Debt-Free

- Use the Spending Pockets: Create a Spending Pocket for each debt, for example, "Credit Card Debt Payment."

- Reason: Using the Spending Pocket allows you to immediately set aside dedicated funds for debt repayment, ensuring they don't mix with other needs. This helps you focus and stay disciplined.

- Baby Step 3: Build a Strong Foundation

- Use the Saving Pockets & Jago Term Deposits: Continue saving funds in the Savings Pocket until you reach the target of 3-6 months of living expenses. After that, move the funds to a Jago Deposit.

- Reason: The Jago Term Deposits offer optimal interest and the funds can be withdrawn at any time without penalty, making it the perfect place to store the family fund that serves as the foundation.

- Baby Steps 4 & 5: Small Drops Become an Ocean & Small Step, Big Leap

- Use the Saving Pockets: Create two separate Saving Pockets: "Retirement Savings" and "Children's Education Savings." Set aside funds from your monthly combined income into these Pockets regularly. To make it easier, use the automatic budgeting/saving feature in the Jago application.

- Reason: Automated saving eliminates the hassle of manual saving every month. Having separate Pockets ensures each fund has a clear purpose and doesn't get mixed up.

- Baby Step 6: Roof Paid Off, Door Opened

- Use the Shared Pockets: Create a Shared Pocket named "Home Mortgage Installment."

- Reason: Home installments are the biggest expense shared by the couple. Using the Shared Pocket makes the fund flow clearer and transparent, allowing you and your partner to see the funds collected and ensure the installment is paid on time.

- Baby Step 7: Rich in Wealth, Rich in Meaning

- Use the Spending Pockets for donations: Create a Donation Pocket for routine giving.

- Reason: Allocating dedicated funds for charitable or social activities helps give a bigger purpose to the wealth you build. This Pocket serves as a reminder that the ultimate goal of financial independence is to do good and make a positive impact.

Quick Q&A About Finances for Newly Married Couples

1. Who should manage the family finances?

Ideally, both should. Managing finances together can be done easily and practically using the Jago Shared Pocket. The goal is to build trust and transparency. You and your partner can view every transaction and make financial decisions collaboratively.

2. When is the best time to start saving for a child's education fund?

The best time is now. Even if you don't have children yet, every rupiah set aside today will have a multiplied value in the future, thanks to the power of compounding.

3. What is the best way to pay off debt?

The snowball method is effective. Pay off the smallest debt first, then use the money that was previously paying off that debt to pay off the next debt. This momentum will keep you more motivated.