Managing a family or household budget is important but not easy to do. If financial management does not go well, financial problems can arise.

According to Islamic finance specialist Greget Kalla Buana, marriage is not just about sharing goals, desires and ambitions. Spouses must also share financial resources (assets, liabilities, etc.). To start managing the family budget with your spouse, there are 4 ways you can try.

4 Ways to Manage a Family Budget

1. Calculate your total income

Before starting to create a budget for various expenses, you need to know in advance how much total income you get every month. Since this is to create a family budget, you also need to include your spouse's income.

In addition to the regular income, you also need to include extra or additional income if any. If the amount varies each month, you can put an average.

For multi-income earners, one of Bank Jago Syariah's customers, Jagoan Annisa Nur Fajrina, shares tips for managing money hassle-free.

"You have to be wise in managing your income from side jobs and a fixed salary. So the money doesn’t get mixed up, separate it using the Jago Syariah Pocket. You also need to make an effort to save money to achieve your goals and fulfill your aspirations. Try saving money in the Saving Pocket to avoid improper use of the money," explained Annisa.

Annisa still has some other tips for managing finances. You can read full tips from Annisa here.

2. Make a list of family expenses

Now that you've calculated your total income, it's time to make a list of family expenses. Do not forget to include all family members because every family member must have needs to be met. If later you have more family members, you can adjust the budget.

Regarding the allocation of funds, Greget suggests several options that you can try to follow. For example 40-30-20-10. 40% for necessities of life, 30% for installments, 20% for future (investments, emergency funds, insurance) and 10% goodness. There is also the 1-1-1 budgeting as exemplified by Salman Al-Farisi, the friend of the Prophet Muhammad, which is 1/3 for needs, 1/3 for alms and 1/3 for business capital (savings, investments).

For necessities of life, you can start with the priority expenses to make sure you don’t forget any single one of them. Examples of the priority family expenses are food, transportation, groceries, monthly bills and child's education.

There are fixed and non-fixed expenses. If there are priority expenses whose amount is not fixed, such as groceries, you can provide the best estimate. Over time, the budget can still be adjusted once you learn your spending patterns and get used to budgeting.

If all the priority expenses have been listed, you can start listing other expenses such as savings, entertainment, etc. For other expenses, it would be nice if you could also categorize them by priority level. For example, setting aside money to save as an emergency fund is more important than spending money on entertainment.

3. Subtract income from expenses and see the remaining amount

To make sure all expenses can be met, you need to subtract the total income from the total expenses. How much is left?

If the number is negative, then this means that your total expenses are greater than your total income. If this is the case, then you need to make some adjustments to your expenses. Maybe the entertainment budget can be streamlined a bit, the frequency of eating at restaurants can be reduced, etc.

4. Choose an easy and practical way of managing your family budget

Given that budgeting is a way of managing finances and ensuring that cash flow remains positive, budgeting must be done consistently.

To be able to do so, you can choose an easy and practical way of managing your family budget. If you do budgeting manually by recording everything one by one, you can become overwhelmed and eventually lose your enthusiasm for managing finances.

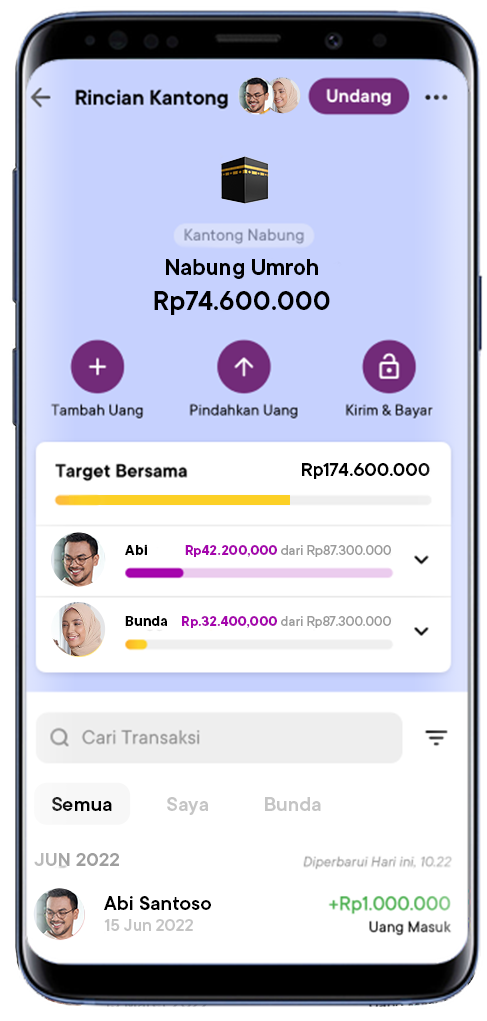

Easy and practical budgeting can be felt when you use the Jago Syariah Pocket. Each need can basically be divided into 2 types, namely the need to save and the need to spend.

Therefore, with Jago Syariah you can create Saving Pockets and Spending Pockets. You can separate every need and allocate a budget into each Pocket.

How many Pockets can be created? Up to 40 Pockets. The cool thing is, each Pocket has its own Pocket number (account number). In other words, you can have 40 different accounts in Jago Syariah.

To manage family budget with your spouse, you can create a Shared Pocket. A number of Shared Pockets is also possible, if you want. Basically, the Shared Pocket is either a Saving Pocket or Spending Pocket. But, when managed by more than 1 person, the Pocket turns into a Shared Pocket.

After you and your spouse are both members of the Shared Pocket, each of you can access the transaction history and perform roles according to pre-defined roles, for example as a spender or only as a viewer. In this way, transparency is maintained by using the Shared Pocket.

Jago Syariah Saving and Spending Pockets Use Wadiah Akad Without Interest in Accordance with Sharia Principles

Managing your family budget can be more blissful with Jago Syariah. Applying sharia principles according to Islamic teachings, Jago Syariah uses Wadiah Yad Dhamanah akad for its Saving Pockets and Spending Pockets. As such, you will not earn interest when saving and managing your family budget at Bank Jago Syariah.

Time to start managing your family budget hassle-free with the Jago Syariah Pocket. Bank Jago Syariah is a sharia digital bank in Indonesia with complete features and a strong ecosystem.