In the journey of life, every one of us surely has long-term financial goals, ranging from disciplined savings planning to investment strategies to ensure funds grow optimally. However, behind all that planning, as a Muslim, have you ever asked the fundamental question: "Are all the steps I take in managing my personal finances aligned with sharia principles?"

Ensuring blessing (barakah) in every transaction is the essence. Amidst the rapid development of sharia financial literacy and digital finance, it is important for us to conduct a financial reflection. This is a proactive step to ensure that our emergency funds, monthly budgets, and entire assets are channeled through an ethical and blessed path, free from elements prohibited by religion.

The Importance of Akad: Fundamental Principles of Sharia Finance

The core of sharia economics lies in the akad or agreement that underlies every transaction. This akad is the fundamental determinant that ensures your transactions are free from interest, gharar (uncertainty), and maysir (gambling). Understanding these two main akad is crucial when choosing sharia financial products:

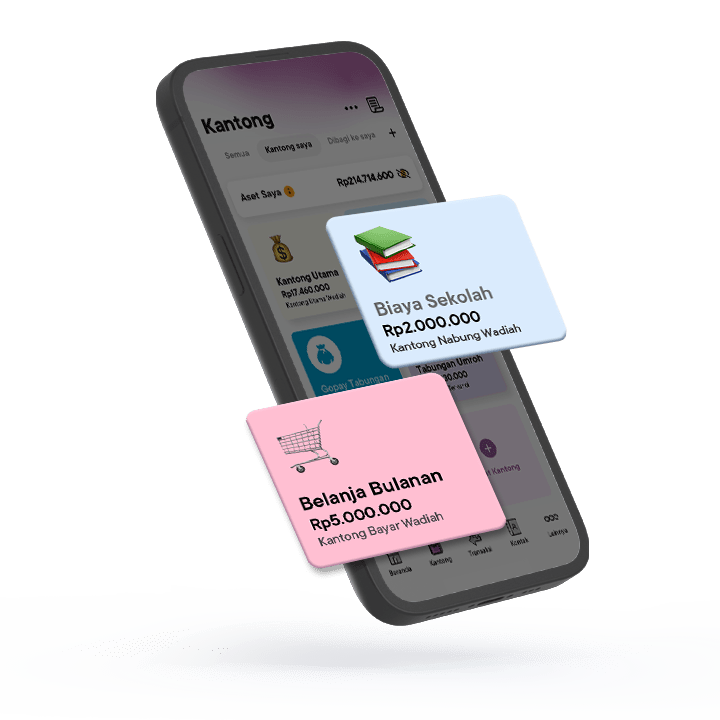

1. Wadiah akad (safekeeping)

This akad adheres to the concept of pure safekeeping. The bank (as the recipient of the money being deposited) guarantees the integrity of the deposited funds. A return is not a condition stipulated upfront, as the primary purpose of this akad is secure storage.

Learn more about Wadiah akad in this article.

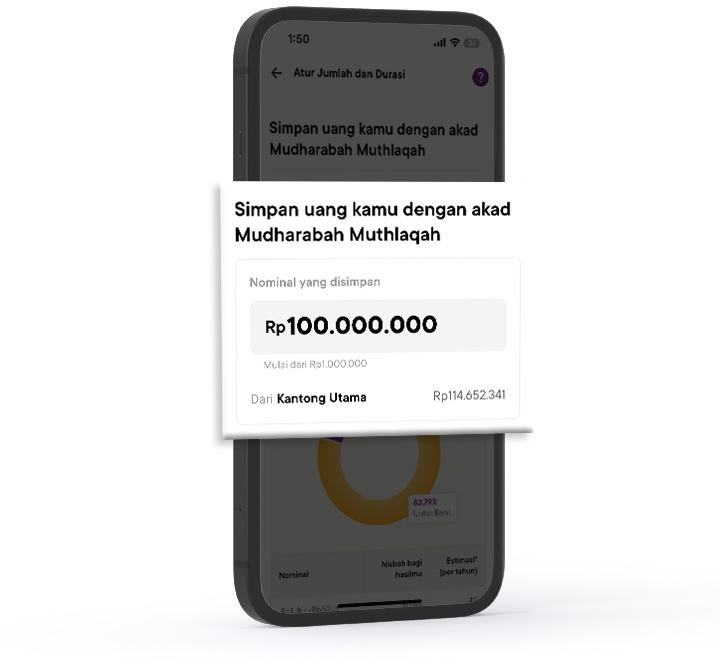

2. Mudharabah akad (profit sharing)

This akad is a cooperation scheme. You (as the shahibul maal/fund owner) provide the funds, and the bank (as the mudharib/manager) will manage them in halal business activities. The profit generated is shared based on the nisbah (profit-sharing ratio) agreed upon at the beginning.

Learn more about Mudharabah akad in this article.

Benefits of Saving Money in a Sharia Bank

Shifting savings and investments to a sharia bank offers dual advantages: blessing (barakah) and clarity.

- Clarity of Akad and Blessing: The primary advantage is the certainty that funds are managed in accordance with sharia principles. By avoiding interest, you ensure that the wealth you possess grows through permissible means (halal).

- Transaction Transparency: Sharia banks operate on the principle of profit sharing (nisbah), not interest, based on the real performance of halal business sectors.

- Ethical Investment: Funds collected by sharia banks are only channeled to business sectors that do not conflict with Islamic principles (for example, not financing alcoholic beverage industries, gambling, or weaponry). This allows you to participate in an ethical economy.

- Stability and Risk Justice: The profit-sharing model (Mudharabah) tends to be fairer because the risks of loss and profit are borne jointly. This differs from the fixed-interest system.

Sharia-Compliant Financial Management Solution with Jago Syariah

Today, owning a modern and easily accessible sharia account is highly feasible. Jago Syariah offers solutions that integrate the sophistication of digital finance with the certainty of sharia akad. Here is an example of how Jago Syariah makes it easy for anyone who wants to stay ahead in saving and managing finances according to sharia principles.

|

Financial Goal |

Jago Syariah Product |

Akad Used |

Function and Benefit |

|

Daily, Short-Term Savings & Budget Allocation for Needs |

Jago Syariah Saving & Spending Pockets |

Wadiah Yad Dhamanah |

Suitable for allocating daily and short-term budget posts. Funds are easily accessible at any time. |

|

Fund Growth (Investment) |

MudharabahMuthlaqah |

Offers halal savings or investment through a profit-sharing scheme. Funds are managed in ethical sectors, and profits are distributed according to a nisbah (ratio) agreed upon upfront. |

By choosing products with clear sharia akad, you ensure that the process of growing your money is aligned with Islamic principles.

Time to Commit to Managing Money According to Sharia

Reflection on sharia finance is not just rhetoric, but a commitment. Start by re-evaluating the savings and investment instruments currently being used. If you haven't yet, now is the time to start managing your finances according to Islamic teachings for long-term financial peace and blessing.

FAQ About Sharia Finance

1. What is the fundamental difference between Sharia Deposit and Conventional Deposit in terms of profit?

Sharia Deposit uses Mudharabah (profit-sharing) akad. Profits come from the real income of halal business activities, distributed based on a pre-agreed ratio (nisbah), not fixed interest.

Conventional Deposit uses an interest system. The return is a fixed interest rate, regardless of the bank's performance.

Learn about the differences between Jago and Jago Syariah in detail in this article.

2. What is meant by nisbah in Mudharabah products, and why is it important?

Nisbah is the ratio or proportion of profit-sharing agreed upon at the beginning between the customer and the bank. This nisbah is important because it forms the basis for a fair and transparent distribution of profits, unlike interest which is set at a fixed nominal amount.

3. Do the Jago Syariah Pockets with Wadiah akad provide returns or interest?

The Jago Syariah Pocket types, namely Saving Pocket and Spending Pocket, use Wadiah Yad Dhamanah (custody/safekeeping) akad, which is primarily intended for secure storage, not profit-seeking. Therefore, Jago Syariah does not promise returns or interest on the money entrusted.