Preparing a legacy is a crucial step in a family's long-term financial planning. More than just dividing assets, it's an act of responsibility and love to ensure the financial future of loved ones after we're gone. Saving for this purpose means every rupiah set aside holds deep meaning, becoming a guarantee for the family's continued well-being.

Goals and Meaning of Saving for a Family Legacy

Saving for inheritance distribution isn't just about accumulating money; it's also about:

- Preventing Conflict: Clearly allocated funds can minimize disputes among heirs later on.

- Financial Protection: Ensuring that heirs have a financial cushion for urgent needs or transitions.

- Ease of Process: With ready funds, the inheritance distribution process can proceed more smoothly and quickly, without the need for complex asset liquidation.

- Positive Legacy: Demonstrating meticulous planning and care for the family, leaving behind a peaceful and orderly legacy.

Calculating and Simulating Fund Allocation for Inheritance Distribution

Start by estimating the total funds you want to prepare and how you wish to distribute them. This helps you set clear targets.

Disclaimer:This inheritance allocation simulation is solely an example for personal financial planning and does not replace applicable inheritance laws (such as Islamic Inheritance Law, Civil Law, or other customary laws) which may specifically govern asset distribution. Always consult with a legal expert or notary for inheritance distribution that complies with prevailing regulations.

Simulation Scenario: Preparing Inheritance Funds in 10 Years

Let's say you want to prepare a total inheritance fund of Rp1,000,000,000 (One Billion Rupiah) within 10 years (120 months). You have one spouse and three children, and you want to allocate reserve funds for administrative costs.

Main Assumptions for Simulation:

- Real Target Value: Rp1,000,000,000 (current purchasing power)

- Saving Period: 10 years (120 months)

- Average Annual Inflation: 3%

- Average Potential Return: 5% per year

1. Calculating the future nominal target (with inflation)

To ensure that Rp1 Billion today has the same purchasing power 10 years from now with 3% annual inflation, you'll need to accumulate:

Rp1,000,000,000 * (1 + 0.03)^10 = Rp1,343,916,379.

So, the nominal fund target that needs to be accumulated in 10 years is approximately Rp1,344,000,000.

Target fund distribution (total Rp1,344,000,000 in the future):

- Spouse: 25% = Rp336,000,000

- Child 1: 20% = Rp268,800,000

- Child 2: 20% = Rp268,800,000

- Child 3: 20% = Rp268,800,000

- Reserve Fund for Administrative & Unexpected Costs: 15% = Rp201,600,000

2A. Monthly deposit simulation (without returns, only inflation):

If you choose to save manually without leveraging potential returns from investments (e.g., only saving in a regular savings account with very low or zero returns), you'll need to set aside the entire future nominal target evenly.

To reach the nominal target of Rp1,344,000,000 in 120 months: Rp1,344,000,000 / 120 months = Rp11,200,000 per month.

Monthly deposit allocation per share (without returns):

- Spouse's Inheritance: Rp11,200,000 x 25% = Rp2,800,000 per month

- Child 1's Inheritance: Rp11,200,000 x 20% = Rp2,240,000 per month

- Child 2's Inheritance: Rp11,200,000 x 20% = Rp2,240,000 per month

- Child 3's Inheritance: Rp11,200,000 x 20% = Rp2,240,000 per month

- Inheritance Reserve Fund: Rp11,200,000 x 15% = Rp1,680,000 per month

2B. Monthly deposit simulation (considering returns):

If you take advantage of a potential 5% annual return from investments like term deposits, you can save a lower nominal amount because the funds will grow.

Using a financial calculator (Future Value of an Ordinary Annuity), the required monthly deposit is approximately Rp9,070,000 per month.

Monthly deposit allocation per share (with returns):

- Spouse's Inheritance: Rp9,070,000 x 25% = Rp2,267,500 per month

- Child 1's Inheritance: Rp9,070,000 x 20% = Rp1,814,000 per month

- Child 2's Inheritance: Rp9,070,000 x 20% = Rp1,814,000 per month

- Child 3's Inheritance: Rp9,070,000 x 20% = Rp1,814,000 per month

- Inheritance Reserve Fund: Rp9,070,000 x 15% = Rp1,360,500 per month

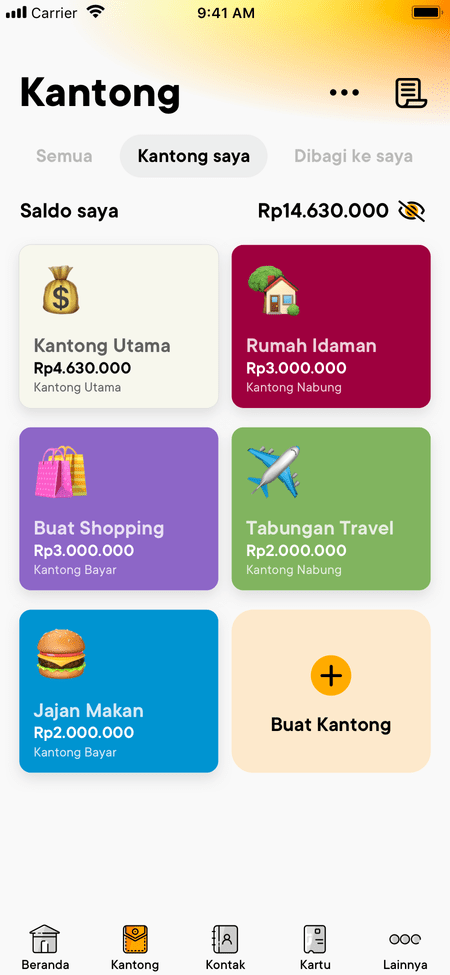

Why the Jago/Jago Syariah Pockets are Perfect for Managing Inheritance Preparation Funds

Once you have an allocation idea, the Jago/Jago Syariah Pockets are here to help you neatly and systematically bring it to life.

The Jago/Jago Syariah Pockets are relevant for managing inheritance funds due to their ease, flexibility, and ability to specifically categorize funds.

1. Specific Pocket creation

You can create separate Pockets for each heir or specific distribution purpose. This is similar to the old-fashioned envelope budgeting method, where each envelope was allocated for a specific expenditure or purpose. With the Jago/Jago Syariah Pockets, you do the same digitally through the application, virtually separating funds for each portion of the inheritance.

2. Clear fund targets

Each Pocket can be assigned a fund target, helping you monitor progress and ensure the desired allocated amount is achieved.

3. Set up automatic inheritance transfers

The automatic budgeting feature ensures consistency in saving, even if you forget.

4. Easy transaction reports

All transactions are neatly recorded, making it easy to track funds and provide transparency.

How to Manage Money for Inheritance Distribution with the Jago/Jago Syariah Pockets

Here are the steps you can take in the Jago application to start organizing the money that will be distributed as inheritance.

1. Identify heirs and needs

- Determine who the heirs will be that will receive a portion of the inheritance.

- Estimate the amount or percentage you wish to allocate for each. Also consider potential costs related to the inheritance (e.g., notary fees, inheritance tax if any).

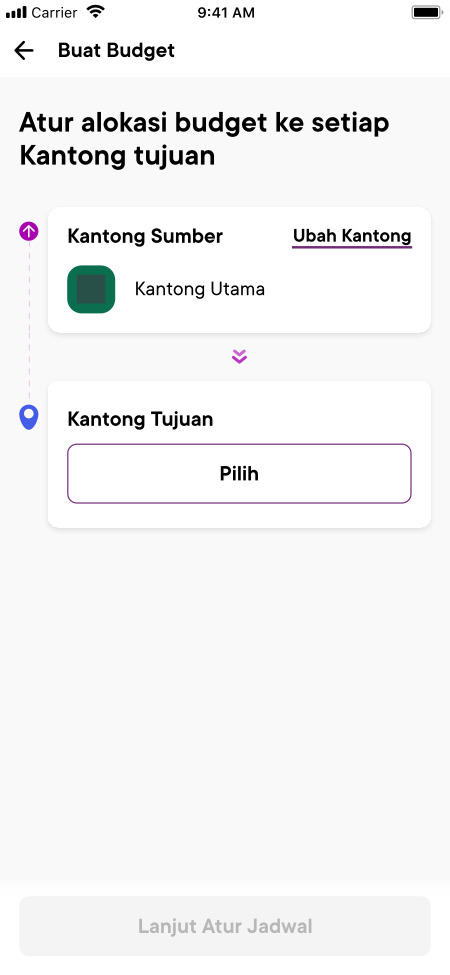

2. Create Inheritance Pockets in the Jago application

- Open the Jago application.

- Create several new Pockets, if following the simulation above: there are Pockets for "Spouse's Inheritance", "Child 1's Inheritance", "Child 2's Inheritance", "Child 3's Inheritance", "Inheritance Reserve Fund".

3. Set targets and automatic saving schedule

- For each Pocket, set a nominal target you want to achieve.

- Activate the automatic saving feature to automatically transfer a certain amount of money to the Inheritance Pockets regularly (e.g., weekly or monthly according to the calculated monthly allocation).

4. Maximizing returns with the Jago Term Deposits/Jago Syariah’s Sharia Deposits

- Once the funds in each Inheritance Pocket have accumulated to a certain amount (e.g., reaching a quarterly or annual target), you can transfer them to a Jago Term Deposit/Jago Syariah’s Sharia Deposit.

- Both deposit products offer competitive returns, so the inheritance funds can grow faster and approach the nominal target that has been adjusted for inflation. Choose a deposit term that suits the planning period, or one that allows you to continue reinvesting the returns.

- Check the latest Jago Term Deposit interest rates here and Jago Syariah’s Sharia Deposit profit-sharing ratios here.

5. Monitor and adjust

Periodically, review the progress in each Pocket and Deposit. If there are changes in financial situations or wishes, you can easily adjust the target or deposit amount.

Questions Regarding Inheritance Preparation with the Jago/Jago Syariah Pockets

1. Can the Jago/Jago Syariah Pockets be used to manage inheritance in the form of non-cash assets (e.g., property)?

The Jago/Jago Syariah Pockets focus on managing cash funds. For non-cash assets such as property, you can use the Jago/Jago Syariah Pockets as a place to collect funds from the sale of such assets or to pay costs related to the inheritance of non-cash assets.

2. What is the difference between saving in the Jago/Jago Syariah Pockets and Deposits for inheritance?

The Jago/Jago Syariah Pockets offer higher flexibility in setting up and withdrawing funds if needed at any time, while still helping maintain saving discipline with target and automatic saving features.

Meanwhile, the Deposits have fixed terms. For inheritance funds that do not need to be accessed within a certain period, Deposits are an option to get more optimal returns.

Maximize Your Inheritance Management Now

Preparing for inheritance distribution is the best investment for peace of mind and your family's future. With the Jago Pockets, you can manage these funds regularly, transparently, and according to your goals. Start planning your inheritance funds today, and give the most valuable legacy: peace and financial security.

For those of you who receive an inheritance, also read: How to Grow Your Inheritance into Financial Strength